Financial infrastructure which drives global commerce has undergone profound transformation. Wholesale payment technology, the systems that facilitate large-value transactions between corporations, financial institutions and government agencies–has grown from paper-based, manual processes to advanced digital networks. Blockchain technology and distributed ledger tech are set to transform the landscape time.

Understanding the evolution of technology helps finance companies, treasury executives and business leaders navigate a complicated payment system. The evolution from clearinghouses to real-time settlements shows how technology is continuing to increase speed as well as security and the transparency of transactions that are high in value.

Why Wholesale Payments Matter More Than Ever

Defining Wholesale Payment Technology

Wholesale payments refers to high-value transfer between banks, corporate, financial institutions as well as government entities. Contrary to retail payments, which people make on a daily basis wholesale transactions typically include billions or millions of dollars in settlement of crucial obligations such as interbank loan or securities purchases. They also provide corporate payroll financing.

The Role of Wholesale Payments in Global Finance

These systems constitute the basis of economic activities. When multinational companies pay suppliers across borders or central banks are conducting operations in monetary policy they rely on the infrastructure for wholesale payments. In the event of a disruption to these systems, it can cause ripple effects across all financial systems.

How Technology Has Reshaped Financial Infrastructure

Every technological advancement in technological advancements in wholesale transactions has led to advances in speed, effectiveness as well as risk control. From reducing days-long delays in settlement to allowing instant cross-border transfers technology continues to revolutionize the boundaries of what is possible in financial transactions.

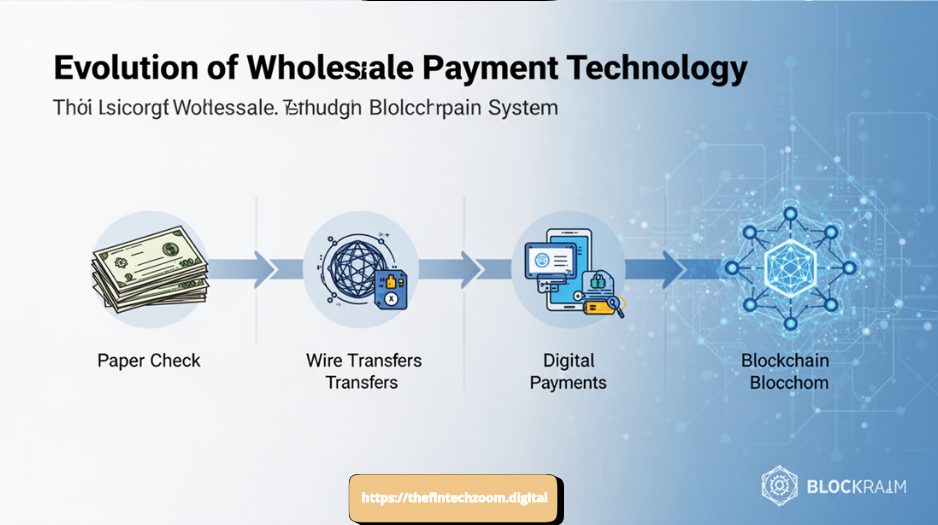

The Early Days: Paper Checks and Manual Clearing Systems

How Paper-Based Payment Systems Worked

Through this century checks made of paper were the main method of wholesale transactions. If Bank A required in order to settle a bill for Bank B the check was sent, mailed, and then manually checked before funds could be transferred. This involved a significant amount of human involvement in every step.

Clearinghouses and the Birth of Interbank Settlement

Clearinghouses came into existence as intermediaries in which banks could swap cheques and balances. Instead of each bank having representatives sent to every another institution in the world, these clearinghouses were able to meet in a central place. This simplified the process, but did not eliminate the need for the exchange of physical documents.

Limitations of Check-Based Wholesale Transactions

Paper-based systems presented significant difficulties. Settlement can take several business days, causing uncertainties in liquidity. Physical checks can be stolen, lost, or changed. Reconciliation requires manual labor intensive processes vulnerable to human mistakes.

Operational Risks and Delays in Manual Processing

The delay between the time it takes to initiate an order and the settlement led to settlement risk, which is the possibility that one party could not be able to pay the funds following having received goods and services. This friction in operation slowed the speed of transactions and also tangled capital inefficiently.

The Rise of Electronic Funds Transfer (EFT)

Change from Physical Instructions to Digital

The advent of electronic funds transfer was the beginning of a major change in the technology of wholesale payments. Instead of checks that were physically held, instructions for payments were transmitted electronically between banks. This significantly reduced processing time and the physical handling cost.

Introduction of Automated Clearing Systems

Automated clearinghouses (ACH) were created to process electronic payment batches. Financial institutions were able to submit documents that contained several payment instructions. the ACH will sort, then net and then settle. This was a huge increase in efficiency over manual processing.

Early Digital Infrastructure and Its Impact on Banks

Banks have invested heavily in the development of computer systems and infrastructure for telecommunications to facilitate electronic payment. This tech-based foundation allowed the same day settlement of numerous transactions, and increased the reliability of operations compared to traditional methods based on paper.

The SWIFT Revolution in Cross-Border Payments

The Emergence of Global Financial Messaging Networks

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) was founded in 1973 to establish a standard for international payments. Prior to SWIFT banks, they used Telex systems that were inconsistent in their formats, which led to mistakes and delays when transacting cross-border.

Standardization of Payment Instructions

SWIFT introduced standard messages that all the participating institutions could read. This language was standardized, eliminating ambiguity and reduced the risk of operational errors in international wholesale transactions.

How SWIFT Transformed International Wholesale Transactions

Through connecting a multitude of financial institutions across the globe, SWIFT enabled reliable, secure payments for international transactions. Although SWIFT does not directly transfer funds however it acts as a communications layer that allows the correspondent banks to perform transfers.

Security and Compliance Enhancements Over Time

SWIFT continually improved its security protocols to deal with new security issues. SWIFT added features to sanctions screening as well as anti-money laundering compliance and fraud prevention – essential features that are essential to wholesale payment technology in a controlled environment.

Real-Time Gross Settlement (RTGS) Systems

What Is RTGS and How It Works

The real-time systems for gross settlement handle each payment in a single step after it is received, instead of making transactions in batches. This reduces the risk of settlement by guaranteeing immediate, irrevocable settlement of the funds among institutions.

The Importance of Instant Settlement in Wholesale Banking

RTGS was as the standard gold for technology for wholesale payments. Central banks around the world used RTGS–such as Fedwire and TARGET2 in the United States and TARGET2 in Europe to facilitate the instant settlement of transactions that are critical to.

Liquidity Management in RTGS Environments

While RTGS removes risk associated with settlement but it also requires banks to ensure that they have enough liquidity during the day. Advanced tools for managing liquidity assist institutions to optimize their cash reserves while also meeting the obligations of payment in real-time.

Global Examples of RTGS Systems

Major economies have their own RTGS infrastructures: CHAPS in the UK, CHIPS in the US for payments made by private sector companies and similar systems across Asia, Latin America, and Africa. These systems process billions of dollars daily in settlement volume.

The Digital Transformation of Core Banking Infrastructure

Centralized Databases and Core Banking Systems

Modern banks operate on the core banking systems which keep central account and customer databases. These platforms are integrated with payment systems for wholesale to allow automated payments processing, reconciliation and reports.

API Integration and Payment Automation

APIs or Application Programming Interfaces (APIs) permit various systems to seamlessly communicate. Banks utilize APIs to connect their core systems to payment networks, allowing straight-through processing, without the need for manual intervention.

Risk Monitoring and Compliance Technology

Advanced analytics platforms track payment flow in real-time and detect unusual patterns that may suggest laundering or fraud. This technology integration improves compliance while also allowing for faster payments.

The Emergence of Fintech in Wholesale Payments

How Fintech Challenged Traditional Banking Models

Fintech companies came up with innovative ways to use wholesale technology for payment that often use the cloud, mobile applications along with data analytics, to deliver more user-friendly experience that traditional banking platforms offer.

Payment Innovation Through Open Banking

The Open Banking regulations required banks to exchange customer data with authorized third parties via APIs. Fintech companies were able to create payment services using existing banking infrastructure, speeding up the pace of innovation.

Collaboration Between Banks and Fintech Firms

In lieu of solely rival relationships several banks collaborated with fintech companies to upgrade their payment processing technology for wholesale. These collaborations paired the traditional banking institutions’ expertise in regulation and fintech’s flexibility.

Blockchain Technology Enters the Scene

What Is Blockchain in the Context of Wholesale Payments

Blockchain is a paradigm change in the way that the data associated with payments is stored and confirmed. As opposed to a database centrally that is controlled by a single entity Blockchain distributes transaction data among multiple parties who together manage the ledger.

Distributed Ledger Technology (DLT) Explained

Distributed ledger technology falls under a broad term used to describe blockchain systems and other similar ones. In the realm of wholesale technology for payment, DLT enables multiple institutions to keep synchronized records, without the need for the approval of a central authority for transactions.

Smart Contracts and Automated Settlement

Smart contracts are self-executing agreements that have been coded in blockchain systems. In the case of wholesale payments, they could automatically trigger settlement if predefined conditions are fulfilled, which reduces the need for manual intervention and operating risk.

Permissioned vs Public Blockchains for Institutions

While public blockchains such as Bitcoin allow everyone to participate however, financial institutions usually utilize permissioned blockchains in which only authorized parties are able to validate transactions. This way of working balances transparency with the need for controls to regulate operations.

Central Bank Digital Currencies (CBDCs) and Wholesale Applications

Understanding Wholesale CBDCs

Central banks around the world are examining digital currencies as a way to facilitate wholesale payments technology. In contrast to CBDCs for retail that target customers, wholesale versions could aid in payment between banks using ledgers distributed.

Pilot Programs and Global Experiments

Projects such as Project Ubin (Singapore), Project Jasper (Canada), and the Digital Dollar Project (United States) have been testing the wholesale CBDC applications. These studies examine the ways central bank money using blockchain can improve the efficiency of payments.

Impact on Interbank Settlement and Liquidity

Wholesale CBDCs could enable atomic settlement–simultaneous exchange of payment and securities–reducing counterparty risk. They may also be able to provide central bank money that can be programmed that allows conditional payments as well as more sophisticated management of liquidity.

Comparing Traditional Systems vs Blockchain-Based Solutions

Speed and Efficiency

Traditional RTGS systems settle transactions within a few seconds, however they typically operate only during working hours. Blockchain-based wholesale payments can provide 24/7 settlement, and possibly processing transactions much faster thanks to parallel processing through distributed nodes.

Cost Reduction and Transparency

Blockchain eliminates the requirement for intermediaries as well as manual reconciliation. Every participant maintains identical records of transactions, eliminating any discrepancies, as well as the expensive processes needed to fix them.

Security and Fraud Prevention

Traditional systems depend on central security controls. Blockchain’s distributed design means that there’s no single source of failure. The cryptographic verification ensures the integrity of transactions as well as immutable records that provide distinct audit records.

Scalability and Interoperability

Legacy systems manage millions of transactions per day, with the highest degree of confidence. Blockchain networks are continually improving efficiency to handle these volumes. Interoperability–connecting different blockchain networks and legacy systems–remains an active development area.

Regulatory and Compliance Considerations

AML and KYC in Wholesale Payments

The anti-money laundering (AML) as well as know-your-customer (KYC) rules apply regardless of the payment technology. Blockchain-based systems need to include compliance checks, even though certain people believe distributed ledgers will improve monitoring through greater transparency.

Data Privacy and Cross-Border Regulation

The technology used for wholesale payments must be able to navigate various privacy laws across different regions. Blockchain’s transparency may interfere with data protection regulations and lead to the creation of privacy-preserving methods such as zero-knowledge proofs.

Regulatory Sandboxes and Innovation Frameworks

A number of regulators have created sandboxes that allow controlled testing of the blockchain wholesale payment technology. These frameworks assist authorities in understanding new technologies, while also allowing for the development of new technologies under the appropriate supervision.

Cybersecurity in Modern Payment Systems

Evolution of Fraud in Wholesale Transactions

When the technology for wholesale payments became digitalized hackers developed sophisticated hacks. Recent breaches exposed weaknesses in SWIFT banking infrastructure and messaging which prompted industry-wide security improvements.

Security Protocols in Blockchain Networks

Blockchain networks employ cryptographic methods to ensure the security of transactions. Consensus mechanisms make sure that participants agree on the validity of transactions prior to adding entries in the ledger. Multi-signature requirements may require multiple approvals when it comes to large transactions.

Resilience Against Systemic Risks

Distributed systems are often more resilient than infrastructures that are centralized. In the event that one node fails, the system continues to operate. This redundant system protects against technical issues and targeted attacks which could cause a system to be unable to function.

The Role of Artificial Intelligence and Automation

AI in Fraud Detection

Machine learning algorithms analyse patterns of payment to find irregularities that could indicate fraud. The systems become more precise as time passes, and adapt to the latest fraud methods quicker than rules-based methods.

Predictive Analytics for Liquidity Management

AI aids banks to forecast payments and improve liquidity positions. Through predicting when large amounts of money arrive or leave institutions can decrease inactive balances, while also ensuring adequate funds to settle.

Machine Learning in Risk Assessment

Advanced analytics analyze risk of counterparties as well as monitor concentration exposures and detect potential operational issues prior to them disrupting payments processing. This information increases the security of the wholesale payment technology.

The Shift Toward Real-Time, 24/7 Settlement

Demand for Instant Cross-Border Payments

Businesses across the globe increasingly demand instant payment processing in all time zones. Traditional systems that have limited operating hours can cause friction for international commerce, which drives the need for a continuous supply of wholesale payment technology.

Infrastructure Challenges for Always-On Systems

Continuous operation requires a robust technical infrastructure that includes backup systems and automated surveillance and a rapid response capability. Financial institutions have to be able to balance security and maintenance requirements.

Impact on Corporate Treasury Operations

Real-time settlement revolutionizes the management of treasury. Businesses gain instant certainty on the cash position, which allows for more efficient capital allocation. But treasurers need to adjust procedures to the batch settlement cycle.

Cost Implications for Financial Institutions

Infrastructure Investment and Maintenance

Implementing a new wholesale payment system requires a significant investment in the infrastructure security, staff, and education. Maintenance of legacy systems adds on ongoing cost, especially when it is necessary to support both new and old infrastructure.

Operational Cost Reduction Through Automation

Despite the initial cost the automation process reduces long-term operational costs. Less manual processes translate to lower personnel requirements for reconciliation or error correction as well as handling of exceptions.

ROI of Blockchain Adoption

The return on investment of the wholesale blockchain technology for payments is contingent on the number of transactions as well as efficiency improvements in addition to risk-reducing. Early adopters will face higher costs however, they could be competitive due to speed and capacity.

Interoperability Between Legacy and Blockchain Systems

Connecting traditional Banking Infrastructure with DLT

The majority of financial institutions are unable to immediately replace their existing systems. Interoperability software allows blockchain networks to interact with wholesale payment technologies, allowing the gradual transition rather than disruptive replacement.

Hybrid Payment Models

Hybrid solutions combine the strengths of both traditional and blockchain systems. For instance, payment requests may be transmitted via blockchain and final settlement is made via established RTGS systems, making use of both technology and reliability that has been proven.

Challenges in System Migration

Moving between payment methods requires technical sophistication as well as regulatory approval and coordination between multiple institutions. Testing should ensure that there is no disruption to the existing payment channels when introducing new capabilities.

Environmental and Sustainability Considerations

Energy Consumption in Payment Processing

Some blockchain consensus mechanisms, particularly proof-of-work, consume significant energy. This is a cause for concern as financial institutions come under greater pressure to minimize their environmental impact.

Sustainable Blockchain Alternatives

Proof-of-stake, as well as other energy-efficient consensus mechanisms can be used to replace methods that consume energy. Private blockchain networks that are used to make payments wholesale generally consume less energy than cryptocurrencies that are public.

Green Finance and Digital Innovation

Blockchain allows programmable payments that can help support environmental goals. For instance, it can automatically direct money to verified green projects, or by enforcing sustainability requirements when it comes to trade financing.

Case Studies: Real-World Adoption of Blockchain in Wholesale Payments

Bank-Led Blockchain Initiatives

JPMorgan’s Onyx platform handles more than $1 billion daily in wholesale transactions that use blockchain. It is a demonstration of the way established banks are adopting distributed ledger technology to facilitate real-world commercial transactions.

Cross-Border Payment Modernization Projects

SWIFT’s GPI initiative makes use of distributed ledger technology that tracks the movement of payments across borders in real-time and provide transparency that was previously not available in banking correspondents. The hybrid model modernizes the existing infrastructure, rather than completely replacing it.

Lessons learned from pilot programs

Initial blockchain research in wholesale payments revealed that technology alone isn’t enough. It requires a framework for governance as well as legal clarity and business models that encourage the participation of all institutions.

Future Trends in Wholesale Payment Technology

Tokenization of Assets

Blockchain can be used to represent traditional assets such as bonds or commercial paper with digital tokens. The tokenization process could revolutionize wholesale payments because it allows an atomic settlement of both payments and transfer of assets.

Cross-Chain Interoperability

As a variety of blockchain networks develop and connect them, it becomes crucial. Cross-chain protocols could enable payments to seamlessly flow across different ledgers distributed similar to how existing payment networks connect various banks.

The Convergence of AI, Blockchain, and Cloud

Future technology for wholesale payments will likely blend AI to make intelligent decisions as well as blockchain for a more clear settlement as well as cloud computing to provide the development of scalable infrastructure. This combination could result in payment systems that are more efficient than current payment platforms.

The Role of Quantum Computing in Payment Security

Quantum computing could threaten existing cryptographic methods, but has the potential to provide enhanced security. The payment industry needs to prepare for quantum-resistant encryption in order to safeguard all payment systems in the wholesale market from potential threats in the future.

Challenges Slowing the Transition to Blockchain

Technical Barriers

Blockchain networks have to be able to reach speed, latency and reliability that are equal to or surpassing existing technologies for wholesale payments. Limitations in the scalability of certain blockchain solutions create technical obstacles for widespread adoption.

Regulatory Uncertainty

Uncertain or changing regulations regarding blockchain, digital assets and distributed systems can cause hesitation. Financial institutions require clarity on regulations prior to committing to wholesale change in payment technology.

Institutional Resistance to Change

Large corporations are more cautious especially in critical functions such as payments. Inertia in the culture, fear of risk and the investment in current systems hinder adoption, even when new technology has clear benefits.

What the Evolution Means for Businesses and Corporations

Treasury Management Transformation

As the technology of wholesale payments advances corporate treasurers get incredible control and visibility. Automated reconciliation, real-time settlement and programmable payments allow better cash control.

Improved Cash Flow Visibility

Instant payment confirmation eliminates any uncertainty about when funds will reach you. Businesses can maximize working capital without a doubt by reducing the buffers of cash needed to handle settlement timing fluctuation.

Reduced Settlement Risk

Advancement towards the real-time, cryptographically secure wholesale payments reduces operational and counterparty risk. Companies are less vulnerable to delay or payment issues which could cause disruption to operations.

Frequently Asked Question

What is the blockchain payment technology?

Blockchain payment technology leverages a decentralized, distributed ledger to facilitate and record financial transactions securely and transparently. With the help of cryptographic protocols the technology guarantees that transactions are indestructible and authentic without the necessity for intermediaries. Blockchain-based payments are extremely efficient, which allows for instant processing, and also reducing cost of conventional banking system.

What’s a wholesale transaction?

Wholesale payments are large-scale financial transactions usually conducted by institutions such as governments, banks as well as large corporate entities. They are used to resolve the interbank transaction as well as securities trades or large-scale payments for goods and services. Wholesale transactions typically require high amounts of safety, swiftness and reliability due to their substantial significance and effect upon financial system.

What are the 5 most important technology developments in FinTech?

The five major technologies that shape the FinTech sector are:

- Blockchain Technology revolutionizing data security, transparency and efficiency of transactions.

- Artificial Intelligence (AI) and Machine Learning (ML) – Enhancing decision-making by using the use of predictive analysis, detection of fraud and customized financial solutions.

- APIs for Application Programming (APIs) – Facilitating seamless integration between various platforms and financial systems.

- Cloud Computing is a the most cost-effective, flexible technology that can be used for FinTech applications.

- Big Data Analytics Transforming massive data sets into actionable data to improve business performance and increase customer engagement.

What has changed in this payment method?

The system for payment has developed in a significant manner over the years, transforming from barter exchanges and the usage of tangible currency like notes and coins. As the use of digital technology electronic payments were made more common with new payment methods like debit cards and credit card transactions, as well as online banking along with mobile-based payments. Recently, the introduction of real-time payment systems as well as blockchain-based solutions has transformed the speed as well as security and access to transactions. The change is part of a continual effort to improve efficiency, less cost as well as enhanced user experiences. **

What is Wholesale Payments? And What is the difference between them and the Retail Purchases?

Wholesale payments are major-value transactions between companies, financial institutions and government entities, often that amount to hundreds of millions. Retail payments are comparatively smaller transactions such as purchases made with credit cards or peer-to-peer transfer.

Why Are Paper Checks No Longer Suitable for Large-Scale Transactions?

Paper checks can cause delays in settlement risk to operations, as well as excessive processing costs that are not appropriate for modern businesses. Electronic wholesale payments offer security, speedier and transparent options.

How Does Blockchain Improve Wholesale Payment Systems?

Blockchain allows real-time settlement eliminates intermediaries, offers transparency in audit trails, and operates 24/7. Smart contracts make it easier to manage complex payment procedures without the need for any manual intervention.

What Is the Difference Between RTGS and Blockchain Settlement?

RTGS is a method of settling payments in real-time through an intermediary (usually the central bank). Blockchain settlement utilizes distributed ledger technology that lets multiple participants sign off on transactions and keep records without central oversight.

Are Wholesale CBDCs Already in Use?

The majority of wholesale CBDC projects are in testing or pilot phases. There is no major country that has implemented an wholesale CBDC to settle interbank transactions however, a few are moving towards implementing.

What Are the Main Risks of Using Blockchain in Banking?

There are risks associated with technological ineptitude as well as security threats, regulatory uncertainty specifically pertaining to distributed systems and operational issues in transferring from a proven infrastructure.

How Long Will It Take for Blockchain to Replace Traditional Systems?

A complete replacement is not likely in the near-term. Instead, anticipate gradual integration as blockchain-based wholesale payments technology will coexist with and eventually complements traditional systems in the coming decade.

Do Legacy Systems Coexist with Blockchain Technology?

Yes. Interoperability tools allow both the blockchain and legacy systems to exchange information. Many institutions are exploring hybrid strategies that combine the traditional technology and distributed ledger.

The Road Ahead for Global Finance

Key Milestones in the Evolution of Wholesale Payment Technology

The transition from the paper check to blockchain is continuous improvement in speed, security, and efficacy. Every step forward–from clearinghouses to SWIFT and from RTGS to distributed ledgers – builds on previous developments while addressing their weaknesses.

The Future for Financial Institutions

Financial institutions are faced with strategic decisions regarding the investment in wholesale technology for payment. The ones that are able to modernize while preserving operational reliability will be the best placed to meet the needs of customers in a digitally advancing economy.

Final Thoughts on the Digital Future of Global Finance

The technology for wholesale payments will keep changing as new developments come into play. Blockchain represents the present technological frontier, but further advances regarding quantum computing, artificial Intelligence or other technologies that aren’t yet developed will further transform. Institutions that are flexible and invest in the right capabilities, and keep a keen eye on the needs of customers will prosper regardless of the specific technology that prevail.

The shift from checks that are manually written to digital ledgers is a reflection of the greater digitization in financial services. As the technology for wholesale payments improves, it becomes cheaper, faster as well as more transparent, it opens up opportunities for economic models and business models which were not previously feasible.